It’s Time To Look Under The Hood At Your Bank

Remember the last time you purchased a vehicle? Of course, you do. The relationship we Americans have with our SUVs, trucks, electric vehicles and luxury sedans is personal – and getting a great deal matters.

From safety features to miles per gallon to passenger and hauling capacity, we don’t commit to a new vehicle until we can tick all the boxes. So, when you drive off the lot, you know what you’re getting — a vehicle you can rely on and enjoy.

Now consider how you chose your bank. The fact that several big banks have failed this year (and the year’s not over) begs the question: Are we more diligent selecting a Ford F-150 than the place where we put our hard-earned savings?

As much as we Americans love our vehicles, we trust our banks. In fact, as of March 2023, according to Morning Consult Pro, approximately 70% of us still trust in banks to do what is right. But does that absolve us from being informed consumers? No.

Here’s what’s happening under the hood at your bank regarding deposits. The FDIC is an independent agency created by Congress to maintain stability and public confidence in the nation’s financial system. One of the things it does is insure deposits at insured banks up to $250,000 per depositor, per bank, per account ownership category. Account ownership categories are single accounts, joint accounts, certain retirement accounts, etc.

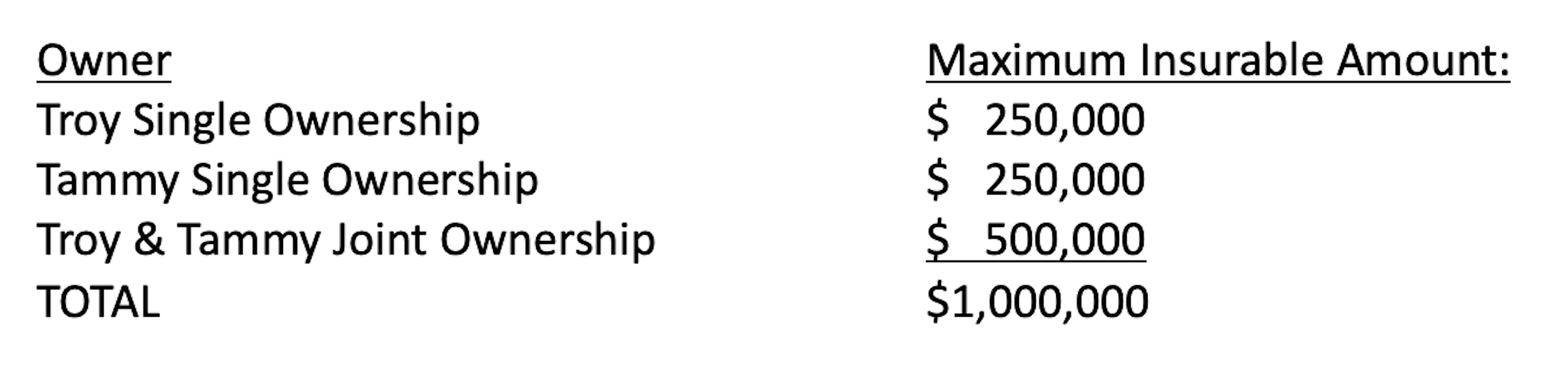

That’s a lot of coverage. By changing the account ownership on some of your deposit accounts, you can significantly increase the amount of deposits that are FDIC insured. Here’s an example of how Troy and Tammy can increase their FDIC coverage at their bank.

If this is news to you, your bank isn’t keeping you informed at the level you deserve.

If diversifying account ownership isn’t enough FDIC protection at your bank, there is another easy-to-get option.

At VeraBank, we use Insured Cash Sweeps (ICS) to put your over-threshold funds in demand deposit accounts or money market deposit accounts and/or Certificate of Deposit Account Registry Service (CDARS) to select CDs from outside sources with term options to meet your needs. The best part is that you can get coverage from multiple institutions through a single relationship. Right here at VeraBank.*

If your bank hasn’t suggested options for you to increase your insured deposit safety, shame on them. Better yet, your bank should be continuously managing risk by minimizing uninsured deposits.

At VeraBank, we have always understood the importance of good liquidity and risk management. VeraBank is funded with stable local deposits from the communities in which we do business and not the kind of “hot” and unreliable money that has brought several banks to the attention of the FDIC and news media this year.

Here’s the takeaway: Our world is changing and although you still can’t beat the advantages a full-service bank offers, you need to check under the hood to make sure your financial security is on a road as smooth as your new car.

Come pop the hood with VeraBank. You’ll like what you see.

This article has been republished with permission. View the original article: It's Time To Look Under The Hood At Your Bank

Disclaimer

While we hope you find this content useful, it is only intended to serve as a starting point. Your next step is to speak with a qualified, licensed professional who can provide advice tailored to your individual circumstances. Nothing in this article, nor in any associated resources, should be construed as financial or legal advice. Furthermore, while we have made good faith efforts to ensure that the information presented was correct as of the date the content was prepared, we are unable to guarantee that it remains accurate today.

* Placement of funds through the ICS or CDARS service is subject to the terms, conditions, and disclosures in the service agreements, including the Deposit Placement Agreement (“DPA”). Limits apply and customer eligibility criteria may apply. In the ICS savings option, program withdrawals are limited to six per month. Although funds are placed at destination banks in amounts that do not exceed the FDIC standard maximum deposit insurance amount (“SMDIA”), a depositor’s balances at the relationship institution that places the funds may exceed the SMDIA (e.g., before ICS or CDARS settlement for a deposit or after ICS or CDARS settlement for a withdrawal) or be ineligible for FDIC insurance (if the relationship institution is not a bank). As stated in the DPA, the depositor is responsible for making any necessary arrangements to protect such balances consistent with applicable law. If the depositor is subject to restrictions on placement of its funds, the depositor is responsible for determining whether its use of ICS or CDARS satisfies those restrictions. ICS, Insured Cash Sweep, and CDARS are registered service marks of IntraFi Network.